When a pipeline project depends on dependable joining technology, the choice of financing can matter just as much as the choice of equipment. For contractors, distributors, and industrial buyers, butt fusion machine purchases are often long-term investments that affect cash flow, project delivery speed, and profitability. HDPE welding machines are built to deliver precise, durable, and repeatable results, but the upfront cost can still be significant, especially when the project requires hydraulic, manual, or CNC automatic models with customized configurations.

The best financing option is not always the one with the lowest monthly payment. It is the one that fits your project timeline, preserves working capital, and supports your growth strategy. For companies working in water supply systems, gas distribution networks, mining operations, or industrial pipeline installations, financing can make the difference between waiting for capital and starting work immediately.

Key idea: the right financing plan should reduce pressure on your cash flow while helping you secure reliable HDPE welding equipment that matches your pipe diameter range, production needs, and project schedule.

Why Financing Matters for HDPE Welding Equipment

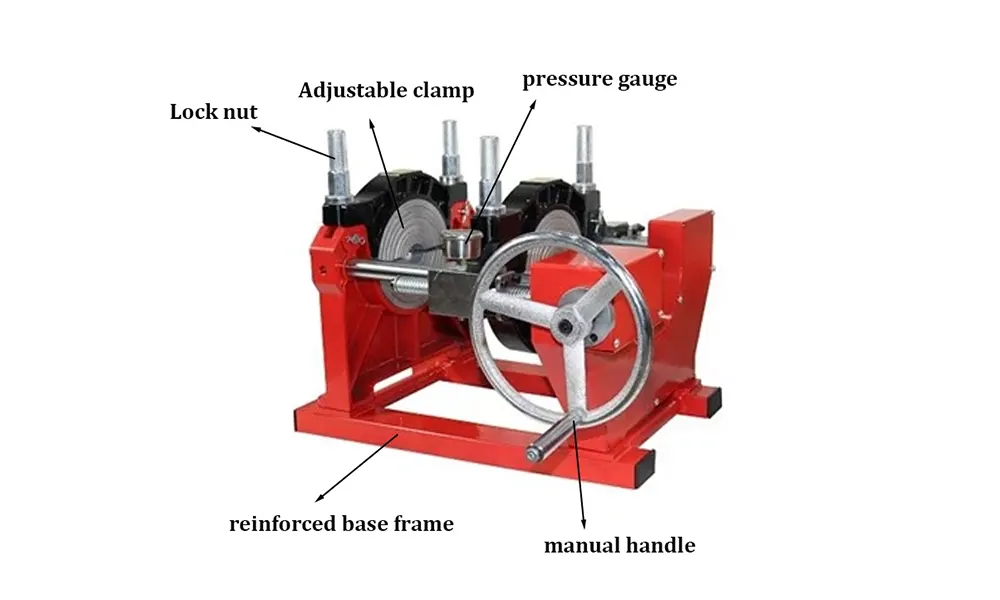

HDPE welding machines are not ordinary tools. They are core assets that directly influence weld quality, installation speed, and field reliability. A poor machine can lead to weak joints, rework, material waste, and costly delays. A high-quality machine, on the other hand, supports stable welding performance and helps teams complete jobs with confidence.

Because of that, many buyers want access to better equipment without locking too much money into a single purchase. Financing provides that flexibility. Instead of paying the full amount upfront, businesses can spread the cost over time and keep funds available for labor, transport, raw materials, and emergency expenses.

Important: if your projects are seasonal or milestone-based, financing can help you align repayments with incoming revenue rather than draining operating cash at the moment of purchase.

1. Equipment Loans: A Traditional and Reliable Choice

Equipment loans are one of the most common financing methods for HDPE welding machines. With this option, a lender provides a lump sum to buy the machine, and the borrower repays it over a fixed period with interest. The machine usually serves as collateral, which can make approval easier compared with unsecured business loans.

For companies that need a durable machine for long-term use, equipment loans are practical because the repayment schedule is predictable. You can plan around monthly payments while still owning the machine from the start. This works well for contractors who want a hydraulic butt fusion machine or a CNC automatic model for recurring pipeline projects.

Best for: established businesses with steady revenue, long equipment life expectations, and a clear need for ownership.

2. Lease-to-Own Plans: Lower Upfront Pressure

Lease-to-own arrangements are attractive for buyers who want to reduce the initial payment burden. Instead of purchasing the machine immediately, the business leases it and makes regular payments. At the end of the lease term, ownership transfers to the buyer, often after a final buyout payment.

This structure is especially helpful for new distributors or contractors entering a market. It lets them begin using a professional-grade welding machine sooner while protecting cash flow. It can also support businesses that want to test a machine model before fully committing to ownership.

JQ-Fusion supports global buyers with flexible OEM and ODM customization, which makes lease-to-own particularly useful when a project requires specific voltage, color, design, or machine configuration. When financing is paired with customization, the equipment can be aligned more precisely with field demands.

Tip: check whether maintenance, service response time, and training are included in the lease package. A lower monthly price is not always better if support is limited.

3. Supplier Financing: Convenient for Direct Buyers

Some manufacturers or distributors offer in-house financing or deferred payment arrangements. This can be convenient because the buyer deals directly with the supplier, which reduces paperwork and shortens the approval process. For project-driven businesses, supplier financing can speed up equipment acquisition and simplify communication.

When purchasing from an experienced manufacturer such as JQ-Fusion, supplier-based arrangements can also be more practical because the buyer can discuss technical requirements at the same time as financial terms. That matters when the project depends on stable temperature accuracy, clamp alignment, and hydraulic pressure stability.

For buyers who prefer working with one point of contact, supplier financing can be an efficient route. It is particularly useful when the project deadline is tight and delays in securing third-party funding would risk missing installation milestones.

Good fit for: buyers who want direct negotiation, faster turnaround, and a closer relationship with the manufacturer.

4. Business Line of Credit: Flexible but Discipline Is Required

A business line of credit gives companies access to funds up to a set limit, and they pay interest only on the amount used. This can be a smart choice if the buyer wants flexibility rather than a single fixed purchase structure. It can also help cover shipping, installation, accessories, or training costs alongside the machine itself.

However, a line of credit works best for disciplined borrowers. Because funds can be drawn repeatedly, it is easy to overspend if project costs are not tracked carefully. For companies managing multiple pipeline jobs, this option can be useful when timing is uncertain but equipment demand remains high.

Reminder: use credit lines for strategic purchasing, not for covering poorly planned expenses. Clear budgeting protects your margins.

5. Project-Based Financing: Designed Around Contract Revenue

Project-based financing is ideal when the machine purchase is tied to a specific contract or pipeline job. In this model, lenders may evaluate the value of the project itself, the client payment structure, and the expected cash inflows. This can be very useful for contractors in water supply, gas distribution, and mining infrastructure, where equipment needs are directly linked to job performance.

This option is especially attractive when the project value is large and the machine will be used intensively over a defined period. It allows the buyer to connect the financing schedule to the revenue cycle of the project rather than relying only on general business cash flow.

For companies building a fleet of machines or expanding into new regions, project-based financing can support rapid scaling without forcing a major one-time capital outlay.

What Buyers Should Compare Before Choosing Financing

Not all financing plans are equal. Before signing, compare the total cost, not just the monthly installment. Interest rate, down payment, term length, penalties, insurance, and support terms can all change the real price of the machine.

Here are the most important factors to review:

Compare these carefully: total repayment amount, down payment, approval speed, ownership structure, early repayment penalties, included warranty, and technical support availability.

Another important factor is the durability and quality control behind the equipment. A machine with strong temperature accuracy and stable hydraulic performance may cost more upfront, but it can save money over time by reducing weld failures and maintenance interruptions. Manufacturers with modern production lines and strict testing processes often provide better long-term value than lower-cost suppliers with limited quality assurance.

Why JQ-Fusion Is a Strong Option for Financed Purchases

When buyers finance a machine, they are not only paying for hardware. They are investing in the ability to complete projects reliably. JQ-Fusion stands out because it combines more than 20 years of industry experience with a broad product range that includes manual, hydraulic, and CNC automatic butt fusion welding machines.

Its manufacturing capability supports customers with different pipe diameter requirements, from smaller installations to large-scale infrastructure work. The company’s strict quality control, modern equipment, and professional technical support are valuable advantages for buyers who need confidence in long-term performance.

JQ-Fusion also offers flexible OEM and ODM customization, which is useful when financing a machine for a specific business model or regional market. Whether the buyer needs a particular voltage, brand style, or functional upgrade, customization ensures the financed asset is not generic but tailored.

In addition, large inventory and fast delivery can reduce costly delays. That matters because financing is only beneficial if the machine arrives in time to generate revenue. A delayed delivery can turn a good financing plan into a burden, so supply reliability should always be part of the decision.

For more information, buyers can explore the manufacturer directly at jq-fusionwelding.com.

How to Choose the Best Financing Option for Your Business

The best financing option depends on your stage of growth and project profile. If your business is mature and cash flow is stable, an equipment loan may provide the simplest ownership path. If you need lower initial payments, lease-to-own may be better. If speed matters most, supplier financing can be the most efficient. If flexibility is the priority, a line of credit may be the right tool.

Start by asking three practical questions: How quickly do I need the machine? How much cash can I safely commit now? How long will the machine be used before I need an upgrade?

Answering these questions will help you match financing to real business needs instead of reacting only to short-term price pressure. The best solution is one that supports both operational continuity and future expansion.

Smart buyer mindset: financing should increase your ability to win contracts, not create hidden strain on the business.

Practical Example: Matching Financing to Application

A contractor installing HDPE water pipelines in a growing city may need a hydraulic butt fusion machine quickly to meet a strict schedule. In that case, supplier financing or project-based financing may be ideal because both prioritize speed and operational readiness.

A distributor building inventory for regional sales may prefer lease-to-own so they can preserve liquidity while testing market demand. A larger industrial group managing multiple installations might use an equipment loan to secure ownership and reduce long-term costs.

In each case, the financing choice should reflect how the machine will generate value. A reliable welding machine is not just an expense; it is a production asset that supports quality, efficiency, and customer confidence.

Conclusion

Financing an HDPE welding machine is a strategic decision that can strengthen your business if handled correctly. The best option depends on your cash flow, project timeline, ownership goals, and the type of machine you need. Equipment loans, lease-to-own plans, supplier financing, credit lines, and project-based funding all offer different advantages.

For buyers seeking dependable performance, customization, and global support, working with an experienced manufacturer can make financing more worthwhile. A well-financed machine should help you deliver stronger welds, take on more projects, and grow with confidence.

FAQ

Q1: Is financing an HDPE welding machine worth it?

Yes, if it helps preserve cash flow, secure better equipment sooner, and support revenue-producing projects.

Q2: Which financing option is easiest to get?

Supplier financing and lease-to-own plans are often easier and faster than traditional bank loans, especially for active project buyers.

Q3: Can financing include customized machines?

Yes, many suppliers can finance customized configurations such as voltage, branding, color, and functional upgrades.

Q4: What should I check before signing a financing agreement?

Review the total repayment amount, warranty, support terms, delivery time, interest rate, and any early repayment penalties.

Q5: Why does manufacturer reliability matter in financed purchases?

Because a financed machine must perform consistently over time. Strong quality control and technical support reduce the risk of downtime and repair costs.